When a brand-name drug’s patent expires, the first generic company to file for approval doesn’t just get a head start - it gets a 180-day monopoly. That’s not a bonus. It’s a legal right under the Hatch-Waxman Act of 1984. During that window, the first generic can charge 70-90% of the original brand price and capture 70-80% of the market. But once that clock runs out, everything changes. Competitors flood in. Prices crash. And the market becomes a free-for-all.

How the First Generic Gets Its Edge

The first generic doesn’t just show up and start selling. They have to win a legal battle. Most of the time, they challenge the brand’s patents in court, claiming they’re invalid or not infringed. If they win - or if the brand agrees to settle - the FDA grants them 180 days of exclusivity. This isn’t just a head start. It’s a financial lifeline.Developing a generic drug isn’t cheap. Legal fees alone can cost $5-10 million. That’s why the first entrant needs that exclusivity period to recoup costs. During those six months, they’re the only game in town. A drug that sold for $320 a month - like Crestor - drops to $100 or $120. The first generic makes money. And the brand? They’re watching their profits evaporate.

What Happens When the Second Generic Arrives

The moment that 180-day clock ends, the floodgates open. The second generic enters. Prices don’t just dip - they plunge. The FDA’s data shows that with one generic, prices are at 83% of the brand. With two, they drop to 66%. That’s a 17-percentage-point drop in a single step. And it’s not because the second company is offering a better product. It’s because they’re undercutting.But here’s the twist: sometimes, the brand fights back. Instead of letting the first generic have all the profit, some brands launch an authorized generic - a version of their own drug, sold under a generic label. In 2019, Merck did this with Januvia. On the exact day the first generic hit the market, Merck’s authorized version came out too. By the end of six months, Merck was capturing 32% of sales. The first generic’s market share dropped from 75% to 45%. Revenue? Down 35%.

This isn’t rare. In high-value markets, 65% of brand companies launch authorized generics during the first generic’s exclusivity window. It’s legal. It’s strategic. And it’s devastating to the first mover.

Why the Third and Fourth Entrants Are the Real Game-Changers

The biggest price drops don’t come from the second generic. They come from the third and fourth.With three generics, prices fall to 49% of the brand. With four, they hit 38%. That’s a 25-30% drop between the second and third entrant - the steepest single plunge in the whole cycle. Why? Because by now, manufacturers are fighting over scraps. No one has exclusivity. No one has brand loyalty. It’s pure cost competition.

Companies entering after the first don’t have to pay for patent lawsuits or do full bioequivalence studies. They can piggyback on the work already done. That cuts their development costs by 30-40%. But here’s the catch: they still need to get the drug approved. And that’s where things get messy.

The FDA’s 2022 guidance says that even if you’re copying a drug someone else already approved, you might still need extra testing - especially if it’s a complex drug. That can add 6-12 months to your timeline. Meanwhile, brand companies are filing citizen petitions - formal complaints to the FDA - to delay approval. Between 2018 and 2022, there were 1,247 of these petitions, each delaying entry by an average of 8.3 months.

Manufacturing: The Hidden Bottleneck

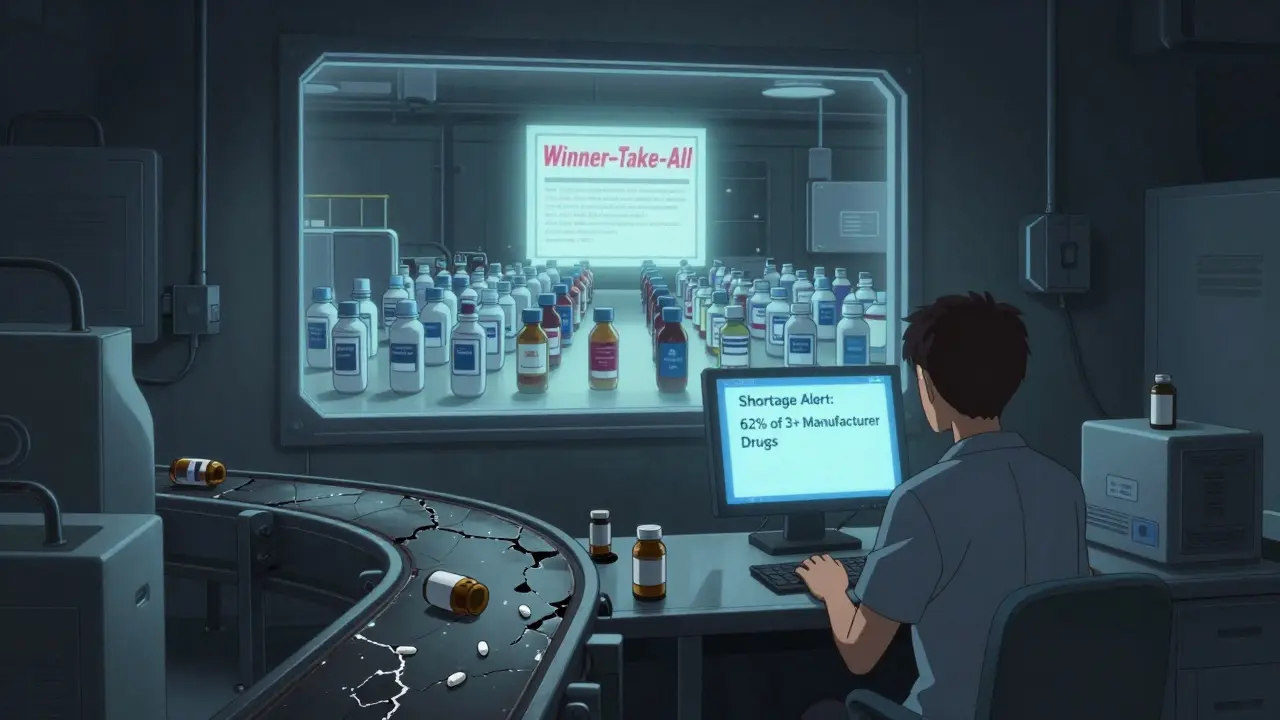

You can get approval. You can win a contract. But if you can’t make the drug, you don’t exist.First generics often own their own factories. They invest millions to build capacity. But second- and third-wave entrants? They outsource. A 2022 FDA report found that 78% of later entrants rely on contract manufacturing organizations (CMOs). Only 45% of first entrants do. Why? Because building a plant is risky. If the market crashes after three competitors enter, you’re stuck with a $50 million factory.

But here’s the problem: CMOs get overloaded. And when they do, shortages happen. In 2022, 62% of all generic drug shortages involved products with three or more manufacturers. That’s not a coincidence. It’s a system failure. Too many companies are racing to make the same cheap drug. No one has the capacity. No one has the incentive to invest. And patients pay the price.

The Rise of the “Winner-Take-All” Contract

Getting approved by the FDA doesn’t mean you’ll sell a single pill. You still have to get onto pharmacy benefit manager (PBM) formularies. And PBMs don’t care who got there first. They care who offers the lowest price.In 2023, 68% of generic drug contracts used a “winner-take-all” model. That means if you’re the cheapest, you get 100% of the business. The others? Zero. It doesn’t matter if you were the first to file. If you’re 5% more expensive, you’re out. That’s why some companies enter the market not to compete - but to be bought. Smaller generics are acquired by bigger ones just to get their approval number.

That’s how the market gets consolidated. In 2018, there were 142 companies holding generic drug approvals. By 2022, that number dropped to 97. The number of competitors per drug fell from 5.2 to 3.8. The market isn’t getting more competitive. It’s getting fewer, bigger players.

How Pricing Stabilizes - And Why It’s Still a Problem

With five or more generics, prices stabilize at around 17% of the brand price. That’s a 90% drop. Sounds great, right? But here’s what happens next:- Cardiovascular drugs (like statins) drop to 12-15% of brand price.

- CNS drugs (like antidepressants) stabilize at 20-25%.

- Oncology drugs stay at 35-40% because they require special handling and storage.

Even at 17%, some drugs are still too expensive for patients. And because manufacturers are barely making a profit, they quit. One company exits. Production drops. Then comes a shortage. Then prices spike again - temporarily. Then another company enters. The cycle repeats.

The Future: Biosimilars and Complex Generics

Not all generics are created equal. Small-molecule drugs - like pills for high blood pressure - are easy to copy. That’s why they have five or more competitors. But complex drugs - injectables, inhalers, creams - are harder. They need specialized equipment. More testing. Higher costs.That’s why complex generics and biosimilars (which copy biologic drugs) have fewer competitors. With two biosimilars, prices are at 70-75% of the brand. With four, they’re at 50-55%. Development costs? $100-250 million per product. That keeps most companies out.

By 2027, experts predict that 70% of simple generics will have five or more competitors - with prices at 10-15% of brand. But for complex drugs? Only 2-3 competitors. Prices will stay at 30-40%. And 40-50% of top-selling drugs will have authorized generics by then.

What’s Broken - And What Could Change

The system was designed to bring down drug prices. And it did. But it also created chaos. Too many companies chase too few profits. Manufacturing gets stretched thin. Shortages become routine. PBMs reward the cheapest bidder - not the most reliable.Some experts, like Dr. Aaron Kesselheim at Harvard, say the system has “perverse incentives.” Too many companies enter too fast. Prices collapse. Companies leave. Patients lose access.

Others, like former FDA Commissioner Dr. Scott Gottlieb, suggest market-based fixes: long-term contracts, restricted entry for simple generics, or even price floors to prevent collapse. But no one has pushed a real solution yet.

The truth? The system works - but not the way it was meant to. It doesn’t guarantee access. It doesn’t ensure supply. It just drives prices down until no one can afford to make the drug anymore.

Releted Post

Caspian Fothergill

Hello, my name is Caspian Fothergill. I am a pharmaceutical expert with years of experience in the industry. My passion for understanding the intricacies of medication and their effects on various diseases has led me to write extensively on the subject. I strive to help people better understand their medications and how they work to improve overall health. Sharing my knowledge and expertise through writing allows me to make a positive impact on the lives of others.

The 180-day exclusivity? Total scam. Big Pharma and the FDA are in bed together. That ‘legal right’? It’s a backdoor subsidy for the first generic-designed to keep prices high until the brand company flips the script with an authorized generic. You think this is competition? Nah. It’s a rigged game where the rules change mid-match. And don’t get me started on citizen petitions. 1,247 of them? That’s not regulation. That’s corporate obstructionism with a FDA stamp.

When we speak of market dynamics we must transcend the mere economic calculus and enter the metaphysical realm where value is not determined by supply and demand but by the hidden architecture of power the patent system is not a tool of innovation but a cage built by capital to imprison access to healing the first generic is not a hero but a pawn in a larger game of attrition where the true victor is the system itself that thrives on chaos and the suffering of those who cannot afford the medicine they need

USA thinks it owns the world’s pharmaceuticals? Let me tell you something-India makes 20% of the world’s generics. We don’t need your 180-day monopoly or your authorized generics. We make it cheaper. We make it faster. And we don’t wait for FDA petitions to start production. Your system is broken because you’re scared of real competition. India doesn’t play by your rules. We just make medicine. And we don’t apologize for it.

OMG this is so eye opening. I had no idea about authorized generics being a thing. Like... why would a brand company do that to their own product? 😵💫 But it makes sense-protect profits by pretending to be the competition. Also the CMO overload thing? Yikes. That’s why we keep having shortages. We need better planning. Like, maybe fund public manufacturing? Just saying. 💡

This breakdown is actually really helpful. I’ve always wondered why some generics are way cheaper than others. The part about winner-take-all PBM contracts explains a lot. It’s not about quality or reliability-it’s pure price dumping. And the fact that companies buy approvals just to sit on them? That’s not innovation. That’s rent-seeking. We need to rethink how we incentivize entry-not just reward the lowest bid.

LOL the first generic thinks they’re winning? Nah. They’re just the first sucker in a trap. Brand companies don’t care about losing market share-they care about cashing out before the crash. And PBMs? They’re just middlemen who don’t give a damn about patients. 17% of brand price? Still too damn high. And don’t even get me started on oncology drugs. 🤡

So the system works… just not for patients. 🤷♂️

It’s wild how the real bottleneck isn’t approval-it’s manufacturing. I mean, we’ve got the science down, we’ve got the regulatory pathways, but we can’t actually make the pills because everyone outsources to the same three factories? That’s like having 50 Uber drivers but only 3 cars. And when one car breaks down? Everyone’s stranded. We need public investment in production capacity. Not just for generics-but for public health. This isn’t just economics. It’s a humanitarian crisis waiting to happen. And we’re ignoring it because it’s ‘too complicated.’

Everyone’s acting like this is some kind of free market. It’s not. It’s a corporate oligopoly with extra steps. The FDA’s ‘guidance’? A joke. The 180-day exclusivity? A loophole. And those citizen petitions? Weaponized bureaucracy. This system was designed to fail. And it did. Now patients are the collateral.